Property foreclosures in Minnesota can be complex, but understanding how the process works across all counties in 2026 helps homeowners, investors, and real estate professionals make informed decisions. Minnesota follows a judicial foreclosure system, meaning foreclosures go through the courts, and procedures may differ slightly between counties. This article explains the Minnesota foreclosure process, county-specific differences, homeowner rights, and tips for investors.

Understanding Property Foreclosure in Minnesota

What is Foreclosure?

Foreclosure is a legal process in which a lender or government authority takes possession of a property after the homeowner fails to meet financial obligations, such as mortgage payments or property taxes. Most Minnesota foreclosures are judicial, requiring court approval. Tax lien foreclosures can also occur if property taxes remain unpaid.

Why Foreclosures Occur

Foreclosures happen for various reasons, including missed mortgage payments, unpaid taxes, or outstanding association fees. Economic changes, job loss, or unexpected financial burdens can trigger foreclosure. Knowing these causes helps homeowners explore alternatives and allows investors to track potential opportunities.

Legal Framework in Minnesota

Minnesota foreclosures follow Minnesota Statutes Chapter 580, which outlines judicial foreclosure procedures. The law ensures homeowners receive proper notice and due process before properties are auctioned. Each county generally follows this framework but may have variations in timelines or auction protocols.

Minnesota Counties and Foreclosure Differences

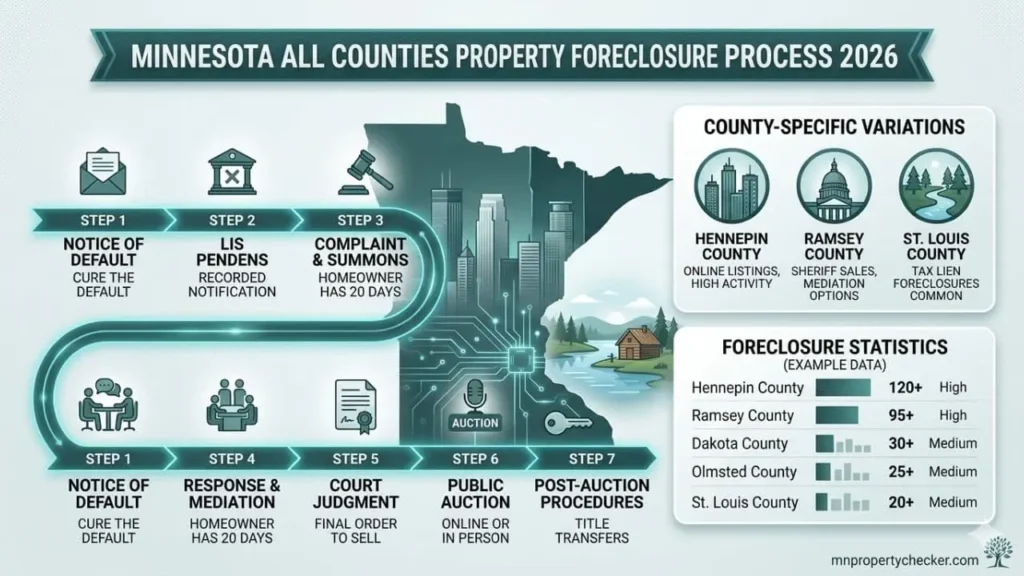

Minnesota has 87 counties, each with slightly different foreclosure procedures and timelines. Some counties process foreclosures faster, while others may have delays due to court caseloads or administrative processes.

Examples:

- Hennepin County – Active foreclosure market, online listings for public auctions.

- Ramsey County – Judicial process with sheriff sale listings; mediation programs available.

- Dakota County – Alternative repayment programs offered for homeowners.

- St. Louis County – Tax lien foreclosures are common; redemption periods apply.

- Olmsted County – Courts process foreclosures efficiently, online auction access.

Understanding county-specific rules is essential for homeowners to meet deadlines and for investors to make strategic decisions.

Minnesota Foreclosure Statistics by County

Foreclosure activity varies across Minnesota’s 87 counties, with some counties seeing higher monthly filings than others. Tracking county-level trends helps homeowners anticipate risks and investors identify potential properties.

County Foreclosure Data Example:

| County | Foreclosures | Activity Level |

|---|---|---|

| Hennepin County | 120+ | High |

| Ramsey County | 95+ | High |

| Dakota County | 30+ | Medium |

| Olmsted County | 25+ | Medium |

| St. Louis County | 20+ | Medium |

| Anoka County | 15+ | Medium |

| Scott County | < 10 | Low |

| Carver County | < 5 | Low |

Step-by-Step Minnesota Foreclosure Process

Step 1 – Notice of Default

The foreclosure process starts when the lender sends a Notice of Default after missed payments, typically 90 days delinquent. This notice gives homeowners a chance to cure the default before legal action begins.

Step 2 – Filing a Lis Pendens

A Lis Pendens is recorded with the county to notify the public that the property is under legal action, preventing the sale or refinance until the foreclosure is resolved.

Step 3 – Foreclosure Complaint & Summons

The lender files a formal complaint in the county court. The homeowner receives a summons and has 20 days to respond. Non-response may result in a default judgment, allowing the lender to proceed to auction.

Step 4 – Homeowner Response & Mediation

Minnesota encourages alternatives like mediation or repayment plans. Homeowners can challenge errors, negotiate adjustments, or request loan modifications to stay in their home.

Step 5 – Court Judgment & Final Foreclosure Order

If no settlement occurs, the court issues a final judgment, allowing the property to be sold at a public auction. All notices and legal requirements must be completed before the sale.

Step 6 – Public Auction

Foreclosed properties are auctioned to the highest bidder. Counties may host auctions online or in person. Bidders typically pay with cash or certified funds.

Step 7 – Post-Auction Procedures

Winning bidders receive a Certificate of Sale. Some Minnesota tax lien foreclosures allow a redemption period, but mortgage foreclosures usually transfer ownership immediately. Title transfers and property management responsibilities follow.

County-Specific Variations in Foreclosure

- Hennepin County: Online auction listings; active investor participation.

- Ramsey County: Sheriff sales with mediation options; judicial timelines vary.

- Dakota County: Alternative programs for distressed homeowners.

- Olmsted County: Efficient court processing; auction notices online.

- St. Louis County: Tax lien foreclosures common; redemption periods apply.

Other counties follow similar steps but may differ in auction procedures, notice requirements, and online access.

Foreclosure Alternatives for Minnesota Homeowners

- Short Sale: Sell property for less than mortgage balance with lender approval.

- Deed in Lieu of Foreclosure: Transfer ownership voluntarily to avoid court proceedings.

- Loan Modification & Repayment Plans: Adjust interest rates or repayment schedules to prevent foreclosure.

Tax Liens & Delinquent Taxes:

Unpaid property taxes may lead to tax lien foreclosures. Counties auction tax liens, allowing investors to collect interest or eventually acquire properties if unpaid. Rules and redemption periods vary, so research local procedures.

Protecting Homeowner Rights

Homeowners have legal protections:

- Right to notice: Must be informed at all stages.

- Right to mediation: Many counties offer alternatives.

- Right to contest errors: Procedural or valuation errors can be challenged.

Avoid scams by verifying the legitimacy of any foreclosure offers.

Tips for Investors Interested in Minnesota Foreclosures

- Research County Records: Know auction procedures and timelines.

- Check Online Portals: Many counties list foreclosure properties online.

- Understand Redemption Periods: Some tax lien foreclosures allow repayment periods.

- Conduct Due Diligence: Inspect properties, check liens, evaluate repair costs.

- Stay Updated: Minnesota foreclosure rules can change; remain informed.

Conclusion

Minnesota’s foreclosure process in 2026 requires careful attention by homeowners and investors. While the state follows a judicial foreclosure framework, county-specific rules, timelines, and auctions make local knowledge essential. Alternatives such as short sales, loan modifications, and mediation help homeowners avoid foreclosure. Investors must research thoroughly before participating in auctions to protect their interests.

Frequently Asked Questions (FAQs)

How long does foreclosure take in Minnesota?

Typically 6–12 months, depending on county and case complexity.

Can foreclosure be stopped after a Notice of Default?

Yes. Homeowners may negotiate repayment, request mediation, or pursue loan modifications before the court judgment.

Are foreclosure auctions public in Minnesota?

Yes. Auctions are public, with many counties offering online participation.

What is the redemption period in Minnesota foreclosures?

Mortgage foreclosures usually transfer ownership immediately. Some tax lien foreclosures allow 30–60 days for redemption.

Do foreclosure procedures differ by county?

Yes. Timelines, auction methods, and mediation programs vary across Minnesota’s 87 counties.